Will video KYC become the norm during and after the coronavirus crisis?

The acceleration towards digital adoption in the banking and finance sector is expected to rise with the introduction of video-based digital KYC as India battles the coronavirus crisis.

Banking and finance plays an essential role in driving the growth of the Indian economy. In the past few years, we have seen the rise of fintechs and digital wallets, which has led to a massive increase in the financial inclusion of the Indian population, especially in rural areas.

To prevent fraud and money laundering, the BFSI sector needs to comply with KYC norms that were introduced by RBI and are based on the Government of India’s (GOI) PMLA Law of 2002.

Aadhaar-based KYC verification had simplified the process and reduced the time taken by the BFSI sector to on-board customers drastically. But, things changed with the Supreme Court order dated September 26, 2018, declaring the use of -based KYC by private players as unconstitutional.

To overcome this challenge, RBI has introduced Video KYC as an alternate tech-driven mode of KYC in its notification dated January 9, 2020. It is based on the Aadhaar and Other Laws (Amendment) Bill, 2019, which was introduced by the government on June 24, 2019.

The RBI amendments state that “with a view to leveraging the digital channels for Customer Identification Process (CIP) by Regulated Entities (REs), the Reserve Bank has decided to permit Video-based Customer Identification Process (V-CIP) as a consent-based alternate method of establishing the customer’s identity, for customer on-boarding”.

Contactless on-boarding during COVID-19

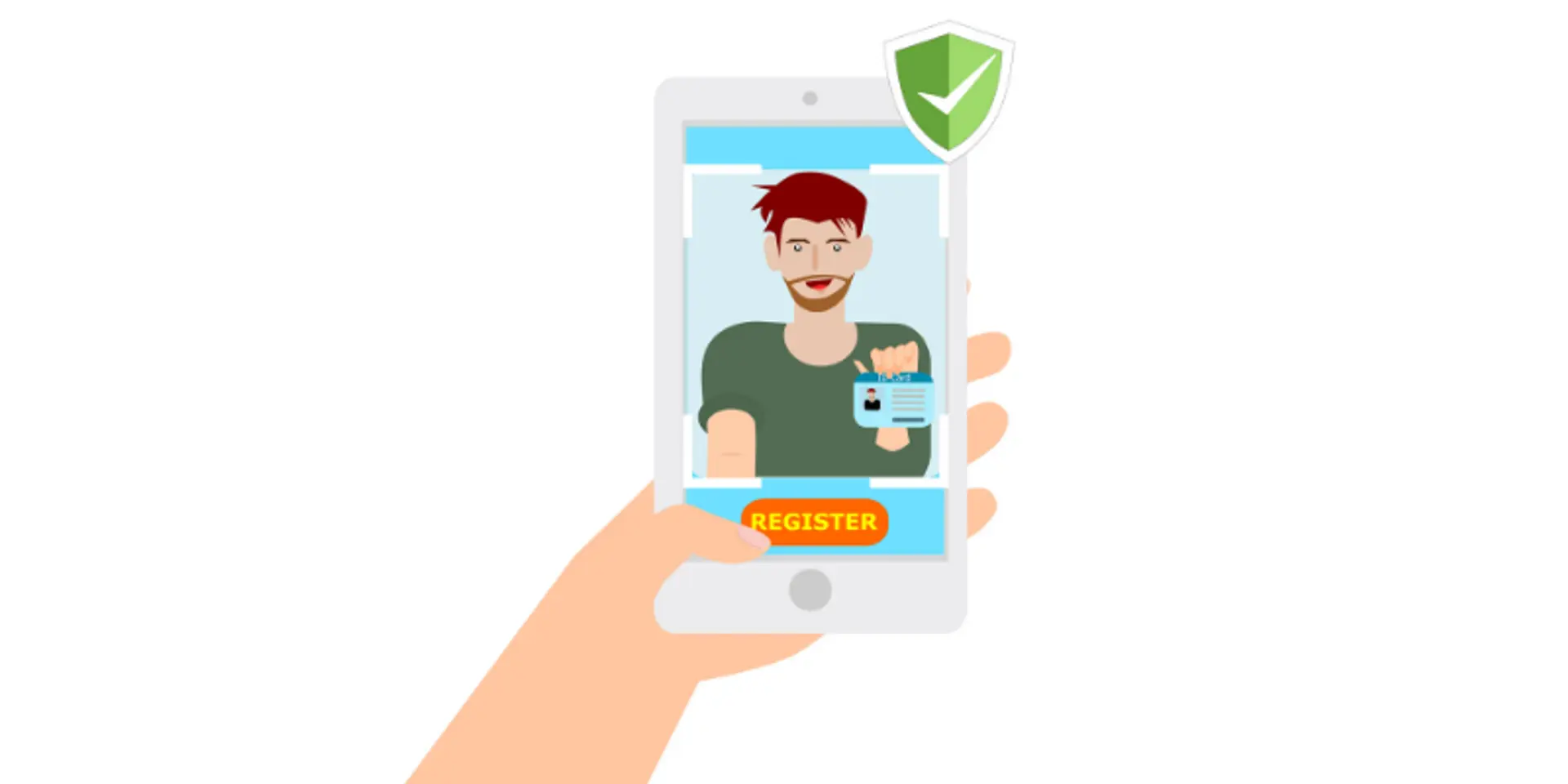

Video KYC could prove to be a tremendous boost for private and public banks, lending companies, prepaid wallet players, insurance, financial securities, and non-banking financial institutions. They are now looking for a contactless and paperless customer on-boarding process while still being 100 percent compliant with RBI guidelines.

The Video KYC provision allows bank officials or regulated entities (RE) to remotely verify the customer’s identity using Aadhaar or PAN card. To ensure the integrity of the Video KYC process, RBI encourages REs to adopt AI-driven and face-matching technologies.

However, there are certain guidelines laid by RBI to comply with before initiating this process. The audio-visual interaction is triggered by RE’s domain, and the Video-Based Customer Identification Process (V-CIP) shall then be operated by the officials that are specifically trained for it.

This could significantly reduce the time from a five to seven-day process to three minutes to on-board a customer remotely. It will allow BFSIs, NBFCs, and e-wallets to provide superior customer experience and will reduce on-boarding costs by 90 percent.

Beyond compliance: a competitive differentiator

While Video KYC has enabled banks to ensure compliance with remote on-boarding, customer drop-offs remain the biggest challenge.

To complete the Video KYC process successfully, customers need to have their Aadhaar, PAN card, and other documents to verify the signature handy. It needs a pre-scheduled time and many times banks would need to chase customers to get this KYC interview to happen.

This then becomes an important step in the on-boarding journey and needs to be looked like a sales funnel.

To ensure higher video KYC completion rates, BFSI companies need to put the effort into reminding and scheduling the video KYC recording at the customer’s convenience. Experience would be key here.

Banking and finance companies that can make this process hassle-free for users have the highest chance to reduce drop-offs and on-board more customers.

Let’s say, for example, a bank ABC uses only outbound calls to remind customers to complete their KYC. Another bank DEF uses other non-intrusive channels, like SMS or WhatsApp, to remind customers and even allows them to reschedule KYC recording on the go.

DEF bank gives the control of KYC completion to the customer who can complete the process at his convenience rather than just getting interrupted by a voice reminder of bank ABC.

This superior customer experience can become a competitive advantage for banking and finance companies to acquire more customers and gain a higher market share.

Future of video KYC

Video KYC is here to stay and will become the de facto choice of customer identification.

We see many tech investments happening in this space to make the system more robust and ensure the integrity of the video KYC process.

Some of these are

- AI-based face recognition

- Ensuring good video quality for low networks

- Video compression to reduce storage space requirement while ensuring integrity

- Fraud and spoofing attack prevention

- Screen sharing for Aadhaar offline KYC

- Concurrent audits to fast-track the process

- Automated omnichannel reminders and schedulers

The acceleration towards digital adoption in the banking and finance sector is expected to rise with the introduction of video-based digital KYC.

While the banking and finance sector has been discussing digital transformation for long, COVID-19 has left them with no option but to implement it. Many of them have started using alternate modes of engagement like WhatsApp and IVR. Video KYC is also enabling them to manage compliance requirements.

The BFSI sector can integrate video KYC as part of the customer journey workflow to on-board customers digitally while still ensuring compliance with RBI guidelines.

Edited by Teja Lele

(Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the views of YourStory.)